The real challenge of the AI age

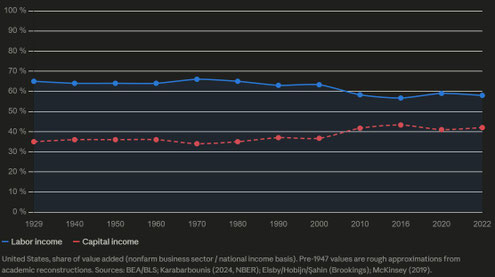

Today, roughly 50–60% of value creation in Western economies still comes from labor, with about 40–50% falling to capital and business income. This ratio shapes nearly every institution in modern economies: the tax system, social insurance, pension models, and even our cultural understanding of merit all rest on the assumption that most people earn their income through work.

But what happens if artificial intelligence permanently shifts that ratio?

The decisive premise

This question could become one of the most important economic policy questions of the 21st century, but only under one condition: that AI doesn't primarily make people more productive, but replaces their labor to a significant degree.

The entire debate hinges on an empirical question: is AI predominantly augmenting or substituting? Does it complement human labor, or replace it? Daron Acemoglu and Pascual Restrepo draw exactly this distinction: the labor share falls mainly when displaced tasks aren't replaced by new, labor-intensive ones. Historically, that replacement has mostly happened in form of the industrial revolution, computerization, and the internet, which all destroyed jobs while simultaneously creating new ones.

The open question, then, isn't whether AI will change work, but whether it will be the first technology to permanently substitute large parts of cognitive labor without generating new tasks for humans at a comparable scale. This article is therefore deliberately framed as a thought experiment: it doesn't describe what has already happened, but the economic consequences that would follow if the substitution thesis turns out to be true.

Every era had to democratize a factor of production

Perhaps we've been looking at the development of modern societies from the wrong angle. In hindsight, one could argue that every major economic transformation forced a new form of social participation in whichever factor of production dominated at the time.

In agrarian society, land was the decisive factor — though its distribution was historically anything but democratic; land reforms were mostly the result of conflict, not insight. With industrialization, the dominant factor shifted to labor. That transition, too, was brutal at first. 19th-century factory work was not democratization but often exploitation. Only over decades, through unions, labor law, and the welfare state, did something emerge that in hindsight can be called the democratization of wage labor. The lesson is an uncomfortable one: such shifts don't democratize themselves, they're fought for.

The 20th century brought further steps — universal education, political participation, and later broad access to knowledge through the internet. But what if AI shifts the dominant factor of production once again? What if, in the future, it's no longer human labor but productive capital, such as companies, AI models, robotics, data centers, data, and intellectual property — that generates the largest share of social value creation?

Then a new historical task may emerge: not the democratization of labor, but the democratization of productive capital. And history suggests that this, too, is unlikely to happen on its own.

The corporate dilemma

For an individual company, maximum automation appears rational: if AI can do the same task more cheaply, faster, and more reliably than people, standard business metrics initially favor substitution.

But what's rational for a single company need not be optimal for the system as a whole. If the labor share falls permanently, the distribution of income shifts — and workers are simultaneously consumers. Depending on how much capital income is reinvested rather than spent, a falling labor share could, over the long run, also weigh on aggregate demand. This connection isn't inevitable, but it's macroeconomically plausible and echoes classic debates about underconsumption and demand. The result is a collective-action problem: every company has an incentive to automate, even though full automation across all companies could have socially undesirable consequences.

Many companies are asking the wrong AI question

Most AI strategies start with a simple question: "How can we use AI to cut as many labor hours as possible?" The more important question might be: "Which tasks should we deliberately not automate, even though we could?"

Not out of nostalgia, but out of business calculation. Companies that automate too aggressively risk three concrete things: the loss of tacit knowledge that only develops through hands-on practice and is missing exactly when systems fail; a shrinking ability to even recognize AI errors, because no one still masters the task manually; and a loss of trust with customers and regulators that can translate into regulatory pushback. The optimal automation strategy is therefore not necessarily identical to the maximum possible one.

The real ownership question

Thomas Piketty ultimately argues that economic stability can only be preserved if wealth doesn't concentrate permanently. But the AI debate shifts this question: going forward, it's less about wealth inequality in general and more about the ownership structure of the specific capital that generates the largest share of social value creation.

That's why the term productive capital is more precise than the general term capital: not gold, not real estate, but stakes in companies, AI infrastructure, robotics, data platforms, and intellectual property.

How could productive capital be democratized?

The answer probably doesn't lie in a single measure but in a combination, and each one comes with its own mechanism, its own funding source, and its own weak point:

Employee capital ownership distributes shares in the company that automates, funded from its profits rather than its wage budget. Its limit: it only helps employees of already-profitable companies, not those who were displaced or never employed in the first place.

National or European citizen funds, modeled on the Alaska Permanent Fund or Norway's sovereign wealth fund, would hold stakes in productive capital and distribute returns to all citizens, funded, for instance, through mandatory levies on IPOs or a digital tax. Their limit is capital flight: a country that taxes capital more heavily than others risks losing investment to other locations.

A stake in the returns of core AI infrastructure follows the same logic as Norway's oil fund, applied to data centers and foundation models. Its limit: the most valuable AI companies are often not based where their returns are meant to be distributed to society.

Shifting tax incentives from real estate to productive capital would extend advantages that currently favor homeownership to broadly diversified stock or fund investments. Its limit is political: homeownership promotion is an established, emotionally entrenched policy goal.

New ownership models for data and digital platforms would give users a stake in the returns generated by the training data they provide. Its limit is technical: there is still no practical method to even measure an individual's data contribution.

Together, these approaches pursue the same idea: if productive capital becomes the most important source of income, its ownership must also be distributed more broadly.

Why a universal basic income alone isn't enough

A universal basic income could secure purchasing power, but it doesn't answer the ownership question. People receive income, but that gives them no stake in the means of production. Economic and political power therefore remains concentrated wherever productive capital sits. In the AI age specifically, this distinction could become decisive: income secures consumption, ownership secures influence.

The real political problem

Even the most compelling models run into the same limit: capital is internationally mobile. A single country can only tax or regulate productive capital differently to a limited degree without risking a loss of competitiveness. Democratizing productive capital will therefore likely only succeed through international cooperation at the European level, for instance, or through new multilateral agreements, similar to the OECD's global minimum tax logic.

Conclusion

Perhaps we've been discussing AI in the wrong categories so far: productivity, prompt engineering, automation, new jobs. The real historical question might be a different one.

Industrialization democratized labor through detours and struggles. The knowledge society democratized education and information. If AI does shift the dominant factor of production from labor to productive capital, the next societal task might be: not the democratization of labor, but the democratization of productive capital.

Whether this actually becomes necessary depends on whether AI predominantly complements or replaces labor. If the substitution thesis proves true, this would be more than a technological revolution, it would be a new ownership question, and, if history is any guide, one that won't resolve itself.